Mutual Funds are essentially a financial intermediary. It is through a mutual fund, that a small investor invests their savings into market instruments like stocks, bonds, treasury bills, debt funds etc. A fund is ‘mutual’ as all its returns minus its expenses are shared by the fund’s investors[1]. The money raised from investors is pooled into a common fund established as a trust which is then invested into market instruments by the fund managers. These fund managers charge the fund for their services along with other expenses like office space and other miscellaneous expenditures which is charged off from the fund itself and is termed as the fund’s expense ratio. Mutual funds normally invest their assets into the following instruments: –

- Stocks

- Bonds

- Government Treasury Bills

- Short-term debt securities – typically one year (termed as money markets)

- Gold

- Real estate

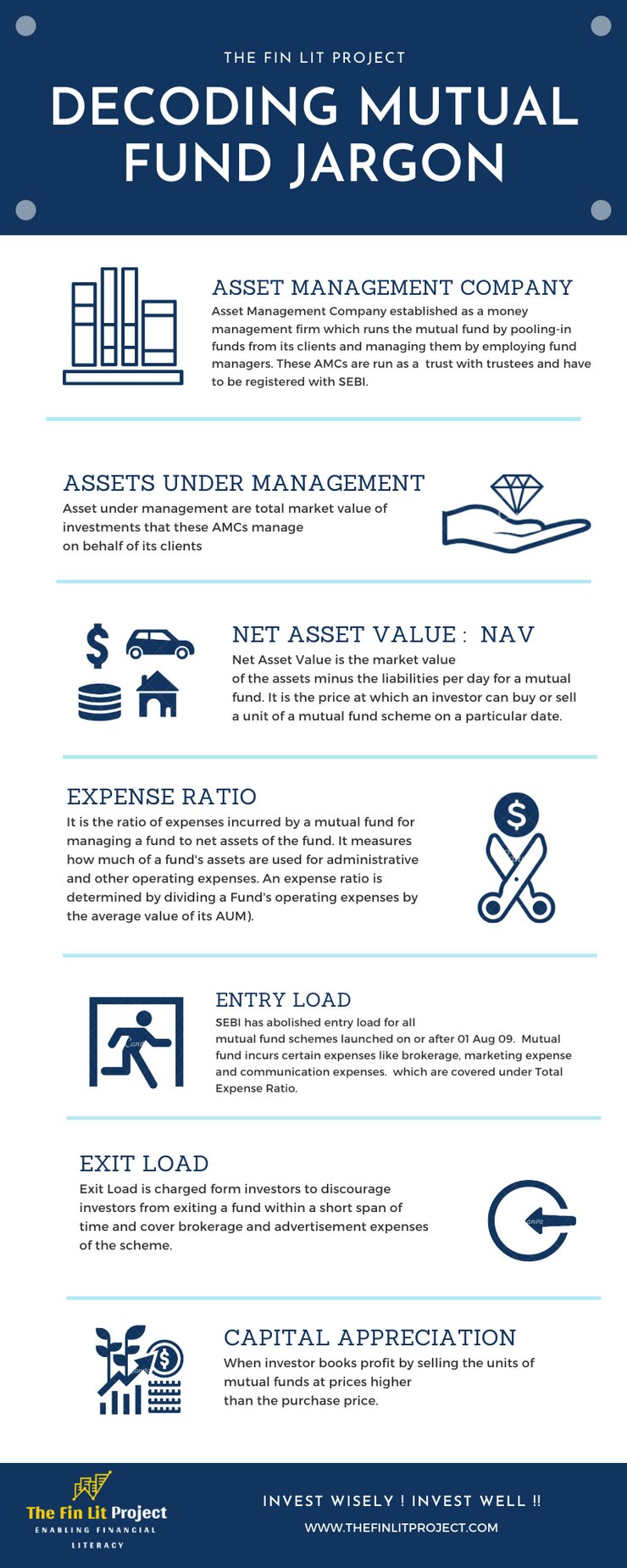

In India, Mutual Funds are constituted in form of public trust under the Indian Trust Act 1882 and regulated by SEBI through SEBI-Mutual Fund Regulations 1996. The SEBI registered Mutual Fund companies termed Asset Management Companies (AMCs) have also established a non-profit association termed as Association of Mutual Funds in India (AMFI) which has 44 members as of date. AMFI aims to develop the Indian Mutual Fund Industry on professional, healthy and ethical lines and to enhance and maintain standards with a view to protecting and promoting the interests of mutual funds and their unit holders[2]. This is the association that airs the ‘Mutual funds sahi hai’ advertisement often seen on television. Some commonly used terms about mutual funds are described below[1][3]: –

Types of Mutual Fund Schemes.:

A Mutual Fund scheme is broadly classified as Direct Plan which is directly purchased from an AMC or Mutual fund house and Regular or Indirect plan which is brought through an intermediary (an advisor, broker or distributor). In a regular plan, AMC pays a commission to the intermediary thereby yielding a lesser return as compared to a direct plan. Depending upon various investment objectives and risk appetite of investors, mutual funds can be broadly classified as follows[1][4]:-

Figure 1: Broad classification of Mutual fund schemes

The details of each classification can be explored using references given in the article. An important point to note is that equity funds offer better returns on investment with associated market risk for a longer horizon. An investor depending upon his requirement profile can look into a balanced and diversified investment into mutual funds. A Systematic Investment Plan ( SIP) route where one invests a fixed sum periodically (say fortnightly, monthly or quarterly) is the best way of investment into the mutual funds however, a retiree willing to invest a lump-sum amount into mutual funds can consider debt funds or enter into equity funds when price-correction occurs in the market.

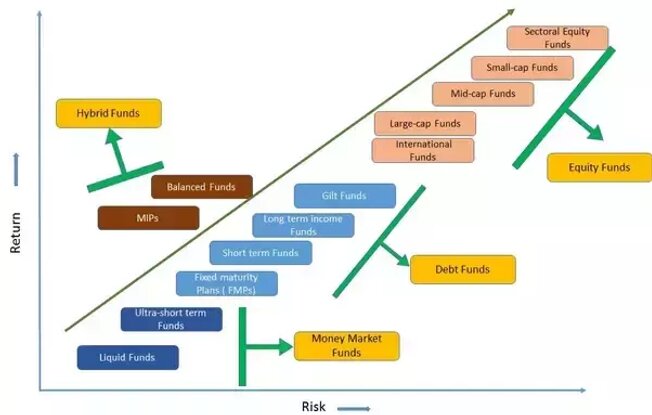

Risk and returns in Mutual funds. Mutual funds are subject to market risk as has been often advertised. Equity-linked mutual funds are directly linked to the market performance of equities in which the Mutual fund AMC has invested. If the markets are not in the upward direction, it can sometimes lead to erosion of capital and negative returns. That said, all the fund managers strive to obtain as high a return as feasible based on the market situation. This leads to the popularity of a scheme and there-by its fund manager. Equity-based mutual funds are riskier as compared to debt mutual funds or arbitrage mutual funds. The proportion of risk varies from type of scheme. Sectoral funds, which invest the funds into a particular industry sector (eg. Pharmaceuticals, automobile, banking, iron & steel, real estate, NBFCs etc.) are riskier as compared to diversified funds. An investor may note that sometimes medium to low-risk options may face liquidity issues and the invested capital might be tedious to obtain a refund. The recent case of winding-up of six fixed income schemes of Franklin Templeton due to illiquidity caused by COVID-19 pandemic in the market is an example of the risk factors associated with mutual funds. The matter is under forensic audit of SEBI and is also sub-judice at Karnataka High Court. A comparative figure of risk vs returns is highlighted in Figure 2.

Figure 2: Risk vs returns for Mutual fund investments[5]

Taxation on Mutual Fund returns. The returns on equity mutual funds after more than a year of investment are taxed @ 10% on returns of over ₹ 100,000 as long-term capital gains tax. For less than a year of investment, the gains are treated as short-term and taxed @ 15% on returns of over ₹ 100,000. For Debt Mutual funds, if investments are realised in less than three years, any gains are added to income and are taxed as per income-tax slab rates (if one is in higher tax bracket, gains would be taxed @ 30%). If investment realization is after three years of investment, returns are treated as long-term capital gains and are taxed at 20% rate with indexation benefits. The indexation benefits help to inflate the purchase cost in an inflationary scenario thereby reducing the gains and bringing down the taxation considerably.

Securities transaction tax (STT) is charged @ 0.025% on sale of a unit of equity-based mutual funds. Trading of units of debt and liquid fund do not attract STT. Dividend distribution tax (DDT) is paid by mutual fund AMCs. However, the investor indirectly bears the tax burden as it is deducted from NAV. This results in lower returns to investors. This tax is applicable to dividend options of debt-based mutual fund schemes.

How to Invest in Mutual fund schemes. Most of the public-sector and corporate banks (SBI, HDFC, ICICI, BoI, IDBI, Kotak Mahindra, UTI etc.) either sponsor a Mutual fund AMC or have their own mutual fund houses. Investor can approach the respective offices of the mutual funds called Investor Service Centers (ISCs) in their own town and cities and fill-out application forms and KYC documents to invest in the scheme. Investment can be made through either the SIP route (payment of fixed amount every fortnight, monthly or quarterly) or as a lump-sum amount. SIP route has its own advantages as it averages out market movements and offers a better average return. Investors can invest in direct plans which give a higher RoI or in a regular plan by utilizing the advice of an intermediary like an agent or a distributor who charges a commission from the mutual fund house. Mutual funds can also be purchased through stockbrokers like Sharekhan, ICICI Direct, India Infoline, Motilal Oswal etc.

Modern discount brokerages like Zerodha, Upstox, 5paisa etc. and platforms like Groww offer the option of utilizing the internet for accessing various mutual fund schemes, analyzing and enrolling in a scheme with minimum paperwork and hassles. For the uninitiated, nowadays banks and post offices also help in the distribution of mutual fund schemes to investors. An investor receives or can seek Key Information Memorandum (KIM) which is provided with the application form and gives information regarding the following aspect of a mutual fund scheme (this gives a better understanding of a mutual fund scheme): –

- Main features and type of scheme.

- Instruments in which the fund has been invested including breakdown of investment as a percentage and absolute value.

- Risk factors.

- Initial issue expenses and recurring expenses to be charged to the scheme.

- Entry & exit loads.

- Sponsor’s track record.

- Educational qualification and work experience of the key personnel including fund manager.

- Performance of other schemes launched by fund house in the past.

- Pending litigations and penalties issued (including forensic audits by the regulator).

Conclusion. This article gives a brief overview of mutual fund investments in India. Different types of mutual funds available in the market are dealt very precisely as it is a very vast topic. Author personally prefers Investopedia, SEBI, NSE and AMFI websites. Links for some of them are provided in the reference. With this article, we strive to give the complete picture regarding mutual funds to our readers to help make informed decisions regarding mutual fund investments in India.

Subscribe to The Fin Lit Project and join our community of finance learners to make better and informed financial decisions by Embracing Financial Literacy!

References

- B. V Pathak, INDIAN FINANCIAL SYSTEM, 5th ed. Pearson, 2018.

- “Association of Mutual Funds in India | Indian Mutual Fund Industry.” https://www.amfiindia.com/know-about-amfi.

- “The Definition of Expense Ratio.” https://www.investopedia.com/terms/e/expenseratio.asp.

- “Types of Mutual Funds – Various Types of Mutual Fund Schemes in India.” https://groww.in/p/types-of-mutual-funds/.

- “How to balance risk and returns in a mutual fund decision – Motilal Oswal.” https://www.motilaloswal.com/blog-details/How-to-balance-risk-and-returns-in-a-mutual-fund-decision../1449.